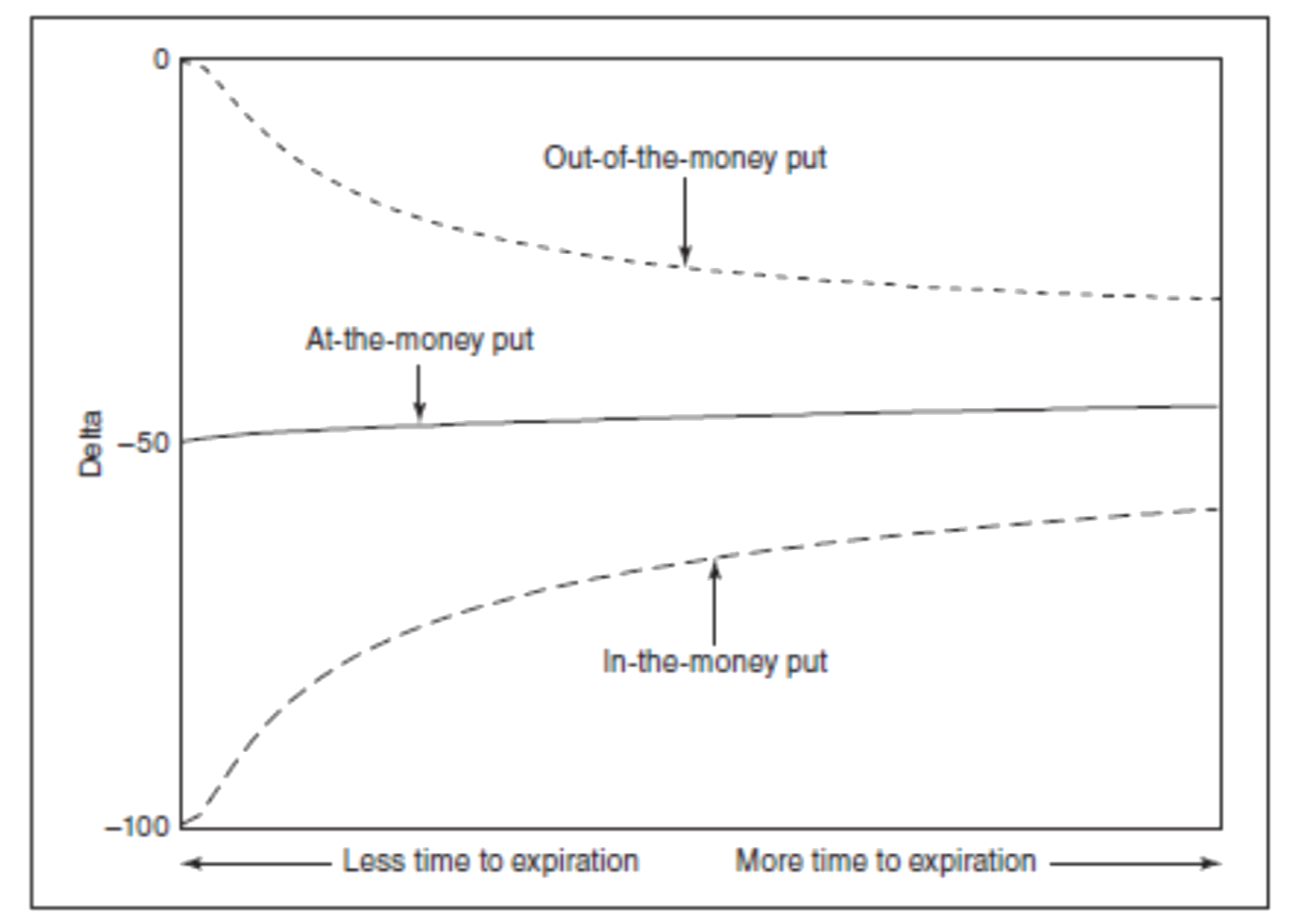

In options trading, the second order option Greek, "charm" (also known as "delta decay") is a measurement of the change in an option's delta due to a change in time to expiration. It is a second-order derivative of the option price with respect to time. The interpretation of charm is that it tells us, how much the delta will change for a one -day decrease in time to expiration.

For example, if charm of a call option is 0.05, it means the delta of the option will increase by 0.05, if there is one-day decrease in time to expiration.

Charm =d(Delta)/ d(Time)

where delta is the option delta and time is the time to expiry.

Charm is an important option Greek because it can help traders manage their delta risk. If a trader has a long call position, for example, the charm is positive, then the delta of the option increases as time passes. This means that the trader may want to hedge their position by selling some of the underlying asset, to offset the increase in delta, in order to maintain a constant portfolio delta.

A negative Charm value means that the delta of the option will decrease as time to expiration decreases. As the time to expiration or days to expiry (DTE) decreases, the option becomes less valuable and more likely to expire out of the money. The Charm is used to measure this rate of change and helps traders manage the risk associated with the passage of time, as mentioned earlier.